Cash flow is one of the most common reasons NDIS businesses struggle, and it's often not just because money isn't arriving on time, it's because the margins are so tight that even when payments do come in, there isn't enough left over to build a meaningful buffer.

The NDIS price guide dictates what you can charge, which means you're working within fixed rates with limited room to move. For a lot of providers, that translates to operating week to week with very little between them and a problem.

When those tight margins collide with the NDIA's two-to-ten-day payment window, a slow plan manager, or an endorsement that wasn't confirmed before support started, the impact is immediate.

The strategies below won't change your rate, but they will reduce the unnecessary cash flow pressure that comes from avoidable admin and process gaps.

Here are the strategies that make the biggest difference.

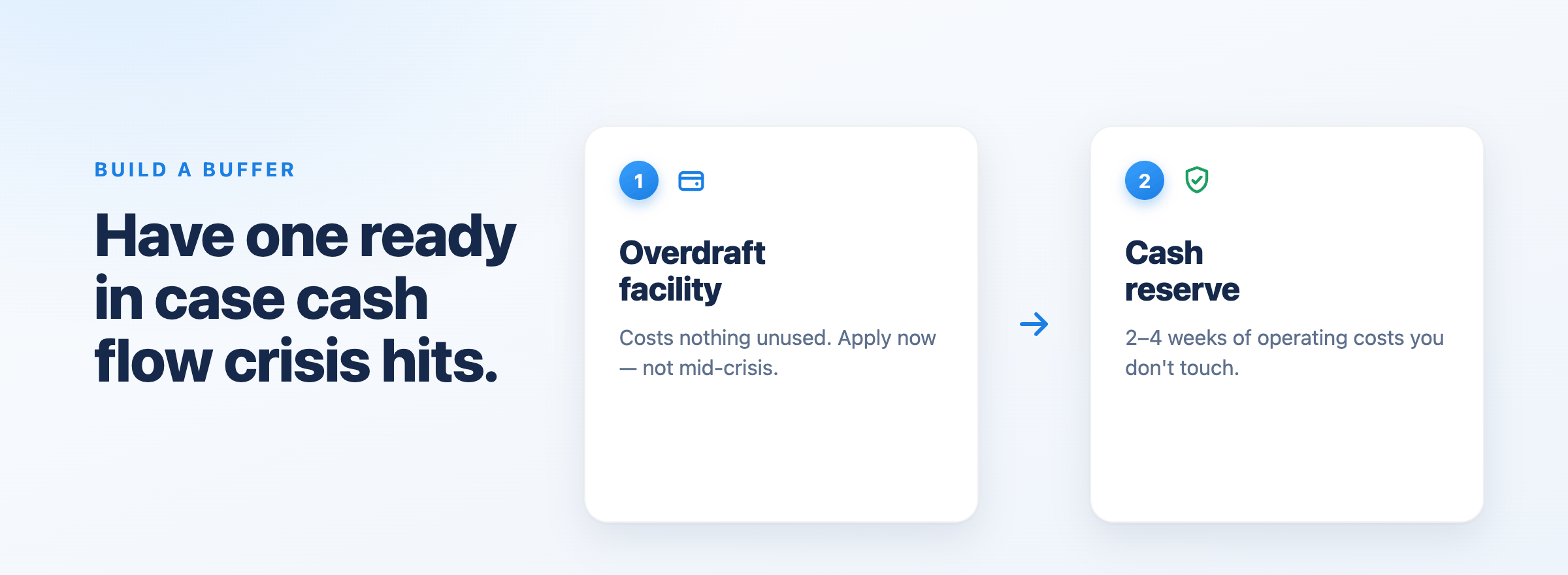

Have an overdraft facility in place before you need it

The NDIA typically processes payments within two to ten days. That's a wide window, and if your invoices consistently land at the later end of that range, the impact on your operating cash can be significant.

An overdraft won't cost you anything if you're not using it. But having one in place means that if the NDIA is slow to process a batch, you're not scrambling. You can still pay your workers, cover your overheads, and keep the business running without interruption.

Apply for it now, not when you're in the middle of a cash crisis. By the time you need it urgently, it's often too late to set it up quickly.

Build a cash reserve

An overdraft is a safety net. A cash reserve is something you own.

Aim to have at least two to four weeks of operating costs sitting in a savings account that you don't touch for day-to-day expenses. Even a small buffer changes the stress levels inside a business significantly. You're not reacting to every payment delay. You're operating from a position of stability.

Build it gradually. Put aside a percentage of each payment received until the reserve reaches your target. Once it's there, leave it alone unless it's genuinely needed.

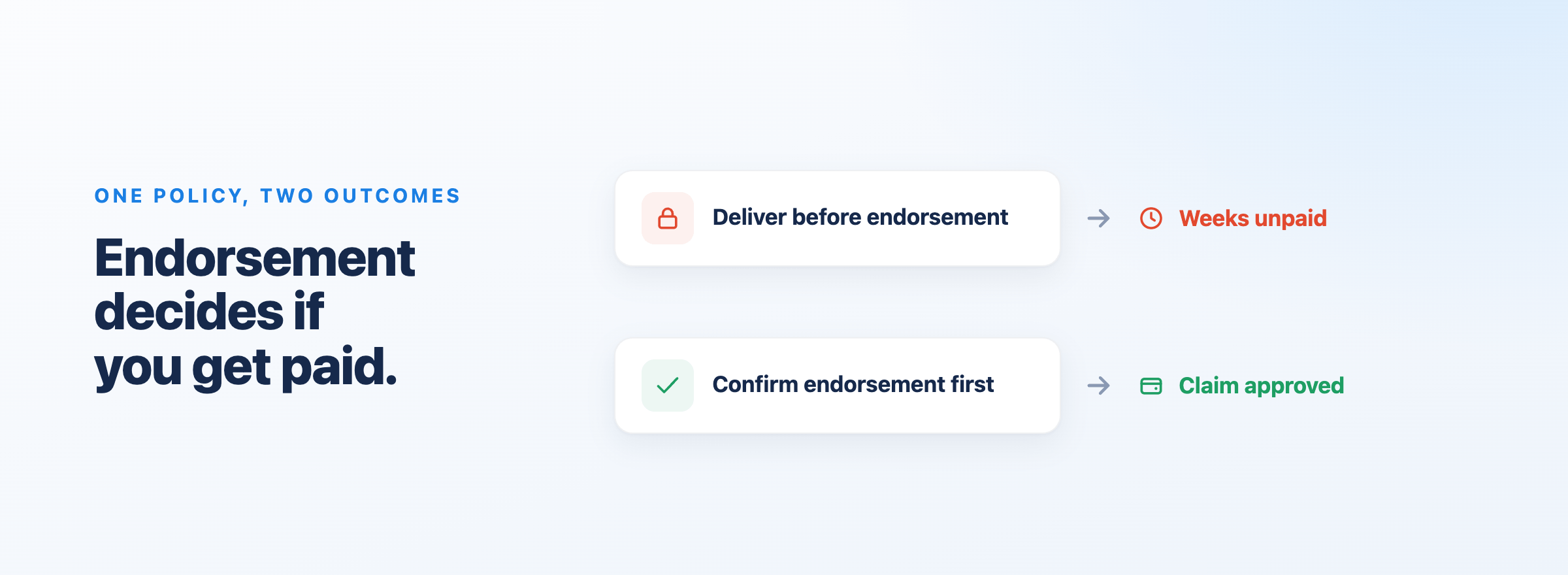

Get your endorsement processes right before you start delivering support

One of the fastest ways to hurt your cash flow is to deliver support without having participant endorsement confirmed. If you're providing services to a participant who hasn't yet endorsed you with the NDIA, you may find yourself unable to claim for weeks or months of work you've already delivered.

The fix is a policy: no support starts until endorsement is confirmed.

Making that policy work in practice means removing friction from the endorsement process itself. That might look like a clear how-to guide written in plain language that a participant or their family can follow step by step. It might be a short video that walks them through exactly what they need to do. The easier the process is for the participant, the faster it gets done, and the faster you can start delivering and claiming your support.

Consider also assigning a team member to track endorsement status for every new participant. If you're carrying a pipeline of participants who haven't completed endorsement, and that situation is happening across multiple people at once, the impact on cash flow adds up quickly.

Be across plan expiry dates

An NDIS plan has an end date, and the real risk isn't invoicing past it, it's delivering support past it.

If you're continuing to roster and deliver services after a participant's plan has expired, you're doing work with no guarantee you'll be paid for it. There's no certainty that the participant's next plan will carry similar funding. There's also no guarantee they'll choose to continue with you once the plan rolls over. Either way, you've absorbed the cost of those services while the outcome is uncertain.

Good participant management software should flag upcoming plan expiry dates well in advance so your team can act, whether that's having a conversation with the participant about their next plan, pausing services until the new plan is in place, or making sure everything is invoiced and reconciled before the expiry date hits. If yours doesn't surface that information automatically, build a manual process: a calendar reminder, a recurring task, whatever it takes to put plan expiry dates in front of you with enough notice to do something about it.

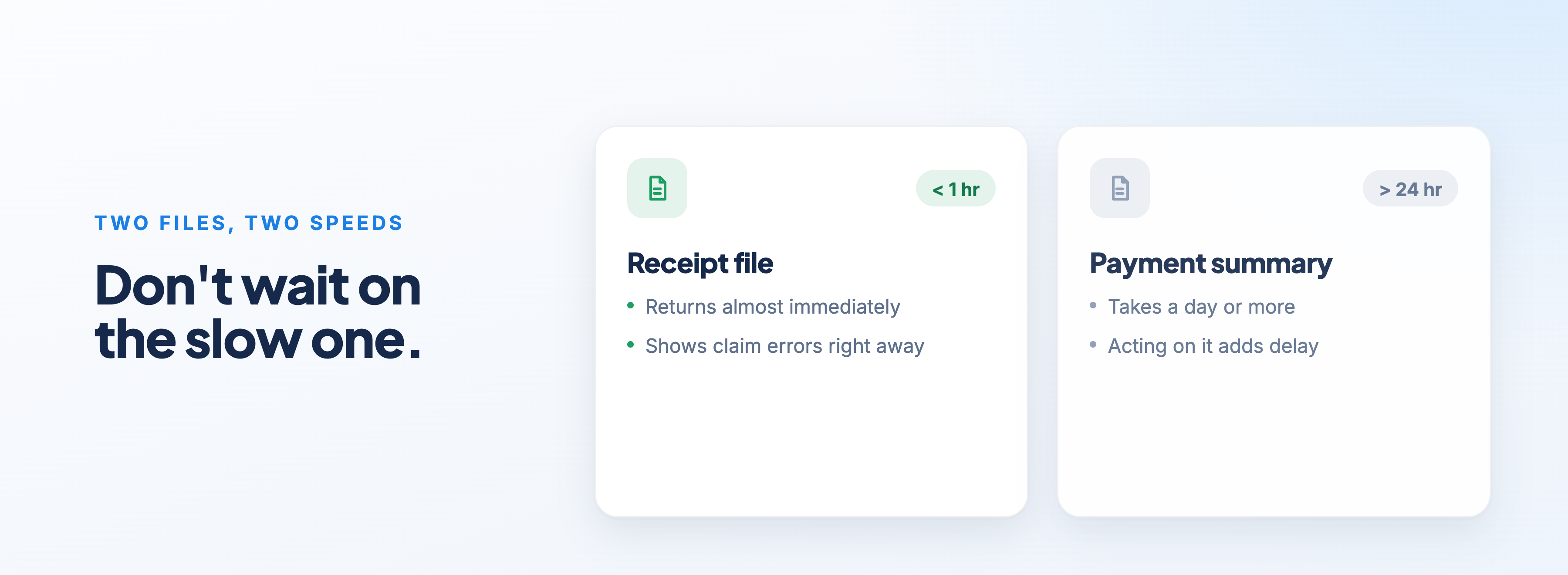

Reconcile your PRODA files quickly

For registered NDIS providers uploading bulk claims through PRODA, the platform returns two files after a submission: a receipt file and a payment summary file.

The receipt file comes back quickly, often within an hour. The payment summary file takes significantly longer, sometimes more than 24 hours.

If your bulk upload contained errors, the receipt file will show you those errors long before the payment summary does. If you wait for the payment summary to review your claims, you're adding at least a day to your error resolution timeline. If you're checking the receipt file as soon as it's available and fixing issues immediately, you're getting paid faster.

The specific error to watch for is endorsement, a claim that comes back rejected because the participant hasn't endorsed you. The sooner you catch that, the sooner you can follow up and resolve it.

Apply strict payment terms for self-managed participants

Self-managed participants pay you directly from their own NDIS funds. That means payment is entirely dependent on them receiving your invoice, accessing their funds, and transferring the money.

Unlike NDIA-managed claims, where you submit and the NDIA pays, or plan-managed invoices, where a professional plan manager is handling it, self-managed payments rely on the participant following through.

Set clear payment terms in your service agreement: 7 or 14 days maximum. Send invoices promptly. Follow up the moment an invoice goes overdue, not after it's been sitting there for weeks. If a self-managed participant is consistently slow to pay, that's a conversation to have early, before the outstanding balance becomes a financial problem for your business.

Reconcile your books daily

The only way to know what's outstanding, and to catch problems before they compound, is to know your numbers. That means reconciling your accounts every single day.

In an age where accounting software and bank feeds are connected, daily reconciliation is not the time-consuming task it used to be. But it does require discipline. If invoices are going out and payments aren't being matched, you need to know about it on the same day, not at the end of the month when you run your accounts.

Chasing a pile of outstanding invoices you didn't know about is significantly harder and slower than staying on top of them as they age.

Don't let your large expenses land in the same month

Some expenses can be influenced in terms of when they fall due. Your workers' compensation premium, your PAYG withholding obligations, your business activity statement, your software subscriptions, look at when each of these lands throughout the year.

If several large expenses are grouped into the same month, that month becomes a cash flow risk regardless of how well the business is performing. Where you have flexibility to spread them out, use it. Talk to your accountant or bookkeeper about your payment schedule and whether there are options to restructure the timing.

If large expenses are unavoidable in the same period, that's exactly the scenario where your overdraft facility earns its place.

Eliminate funding period invoice errors

When a shift or service spans two NDIS funding periods, a plan manager may come back and ask you to split the invoice. That means voiding the original invoice, creating two new ones, and waiting for both to be processed.

Every time that happens, you're adding days to the time it takes to get paid, and you're creating admin for your team.

Good NDIS software handles this automatically. It detects when a shift crosses a funding period boundary and splits the invoice correctly without you having to manage it manually. That's not a nice-to-have feature. If you're regularly dealing with plan manager rejections over funding period crossovers, it's costing you money every time it happens.

Invoice frequently — daily if cash flow is tight

If your cash position is tight, one of the simplest adjustments you can make is to invoice more often.

Invoicing weekly is common. It's also the approach that keeps your money out of your account the longest. If cash flow is genuinely tight, consider invoicing daily.

The mechanics of invoicing are frequently much easier when your software handles batching automatically. You're not manually generating invoices. You're setting a cadence and letting the system run it.

Follow up overdue accounts without exception

Have a process, and run it every time. When an invoice goes overdue, a follow-up should go out the same day, or within a defined window that your team sticks to without exception.

The longer an invoice sits unpaid without contact, the harder it becomes to collect. Most late payments are not disputes. They're delays caused by someone not getting around to it. A prompt, professional follow-up is usually all it takes.

Where invoices are genuinely in dispute, you want to know that early too, so you can resolve the issue and get the invoice reissued and paid as quickly as possible.

Summary

Cash flow problems in NDIS businesses are usually process problems. Payments are slow because endorsement wasn't confirmed before support started. Invoices are outstanding because no one is following up. Large expenses land in the same week. PRODA errors sit unresolved for days because no one checked the receipt file.

The businesses that manage cash flow well are not necessarily the ones with the highest revenue. They're the ones where every step from delivering a support to getting paid is systematised, tracked, and followed through.